Let’s Talk About Fees

Fees matter.

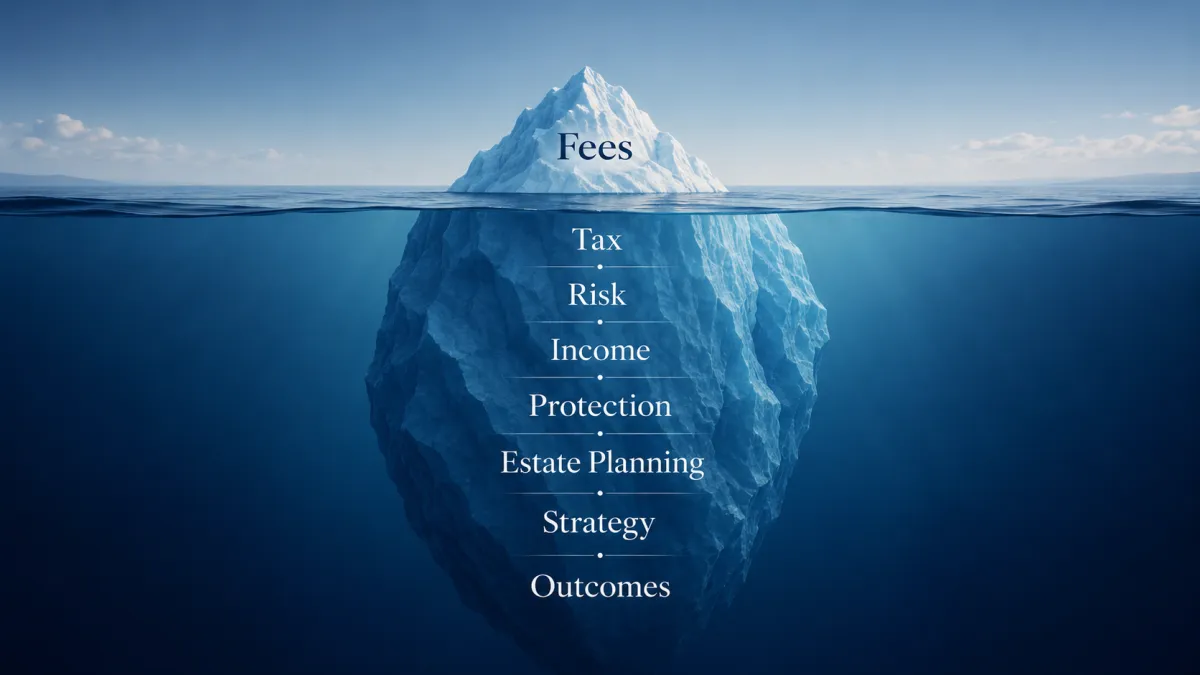

But they are rarely the most important question.

In financial planning, investments, and insurance, the conversation about fees often becomes a false focal point — something that is easy to compare, easy to debate, and easy to obsess over.

But easy does not mean important.

And it certainly does not mean complete.

The real question is not simply: “What does it cost?”

The better question is: “What outcome am I trying to create?”

That is where the real conversation should begin.

When Fees Become a Smokescreen

A fee discussion can be useful. It can also become a smokescreen.

When people focus only on cost, the conversation can drift away from the more important issues: risk, tax, structure, protection, income, estate transfer, family security, and long-term financial confidence.

That does not mean fees should be ignored. They should not.

You should know what you are paying, how you are paying it, and what you are receiving in return.

But when the entire conversation starts and ends with fees, something important gets lost.

A low-cost solution that fails to solve the right problem is not good value.

It is just a cheaper mistake.

The Problem With Starting at Price

Fees are easy to see.

Outcomes are harder to measure.

That is why so many people start with questions like:

“Who has the lowest fee?” “Which product is cheapest “What is the rate?” “How much does the advisor charge?”

Those are fair questions.

But they are not complete questions.

A low fee attached to the wrong strategy is not a bargain. It is simply a less expensive way to arrive somewhere you did not intend to go.

Price Only Matters in Relation to Value

Most people do not actually want the cheapest solution.

They want the right solution at a fair cost.

There is a difference.

If the goal is to protect your family, reduce tax, create retirement income, preserve wealth, fund a buy-sell agreement, or transfer assets efficiently to the next generation, the fee is only one part of the equation.

The more important question is:

“What am I paying for, and what problem is this supposed to solve?”

If the answer is vague, the fee is too high — even if it looks low.

If the answer is clear, measurable, and aligned with the outcome you want, then the fee becomes part of the planning discussion rather than the whole discussion.

Rates Are Often Quoted Net of Fees

One of the most misunderstood parts of the fee conversation is how rates are presented.

In many cases, when rates of return are quoted, they are quoted net of fees. That means the stated return already reflects certain costs associated with managing or administering the investment.

So, when someone says, “I earned 6%,” that return may already be after embedded investment fees have been accounted for.

That does not mean fees should be ignored.

It means you need to understand what is actually being compared.

A quoted return, a management fee, an advisor fee, an insurance cost, and a planning retainer are not all the same thing. They pay for different functions. They show up in different ways. And they should be judged against the value they are intended to create.

The Better Question: What Outcome Do You Want?

When someone is overly focused on fees, I try to bring the conversation back to the desired outcome.

Do you want more certainty? More income? Less tax? Better protection? A clearer estate plan? A more efficient corporate structure? A second opinion before making a major financial decision? A plan your spouse or family can actually understand if something happens to you?

Those are the questions that matter.

Because once the desired outcome is clear, then we can have an honest conversation about the cost of getting there.

Cheap Advice Can Be Expensive

There is a cost to good advice.

There is also a cost to no advice.

And sometimes, there is a very high cost to advice that appears free.

Poor structure, missed tax opportunities, inadequate protection, unnecessary risk, family conflict, probate exposure, liquidity problems, or income shortfalls can cost far more than the fee someone was trying to avoid.

The irony is that many people will spend tremendous energy trying to save a small amount on fees while overlooking planning gaps that could cost them tens of thousands of dollars — or more.

That is not being careful.

That is being distracted.

Fees Should Be Transparent, Not Obsessive

A good advisor should be able to explain how they are paid.

Clearly.

Directly.

Without dancing around the answer.

You deserve to know whether compensation comes from a planning fee, an investment management fee, an insurance commission, a referral arrangement, or some combination of those.

Transparency matters.

But transparency is not the same as making fees the only thing that matters.

The purpose of the conversation should be to understand whether the advice, product, structure, or strategy is appropriate for the result you are trying to achieve.

The Real Test

Here is the real test:

After the fee is paid, are you in a better position?

Do you have more clarity?

Are risks better managed?

Is your family better protected?

Is your income more secure?

Is your tax picture more efficient?

Are your decisions better aligned with your goals?

If the answer is no, the fee was too high.

If the answer is yes, the fee should be considered in context.

Final Thought

Fees matter.

But outcomes matter more.

The fee conversation should not become a smokescreen that prevents you from asking better questions. Nor should it become a false focal point that causes you to mistake price for value.

The goal is not to pay the least.

The goal is to make better decisions, avoid costly mistakes, and create the result you actually want.

So yes, let’s talk about fees.

But let’s not allow that conversation to distract us from the bigger question:

What are you trying to accomplish, and what is it worth to get it right?

Disclaimer: Rates, returns, fees, and compensation structures vary by product, provider, account type, and individual circumstances. Quoted rates of return may be shown before or after certain fees depending on the source and type of investment. Always review the applicable disclosure documents and speak with a qualified advisor before making financial, investment, insurance, tax, or estate planning decisions.